The industry needs to act now to prevent boom-time type problems blighting recovery

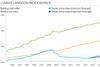

The mercury has been steadily rising over the past week, leaving much of the UK and particularly London and the South-east basking in a heatwave. But with housebuilders expanding output (page 17), the government reporting a surge in house price inflation of almost 7% in London over the last year, as well as steady growth in the rest of the country, it is the housing market that is heating up.

Clearly this is good news for the industry, and will be a welcome break for all those contractors and specialists still reeling from years of falling workloads and vanishing margins. However, that the last month has seen the first signs of a return of boom-time type problems in the housing supply chain: soaring product lead times; lack of availability of tower cranes and piling subbies; day rates for skilled labourers such as brickies shooting up by a third; and contractors walking away from jobs.

Just a few weeks after the launch of a vision for construction in 2025, it is a bit deflating to realise how far the industry has to go

Yes, this is only in one sector, and primarily in one part of the country. But, the fact it is happening at all should come as a stark warning to an industry that risks finding itself back in exactly the same place as it was when the nineties boom started almost 20 years ago. Skills bodies such as the CITB have been warning for some time that we have been storing up trouble by reducing the industry’s skills capacity so far and so fast, and that we’ve been failing to prepare for the upturn by training enough skilled people to meet future demand.

Last time around, Sir John Egan called on the industry to embrace partnering and modern methods of construction. The pressure the inevitable cost rises associated with a rising market put on contractors and specialists on fixed-price contracts, which can easily end in company casualties, can be avoided by a partnering approach to construction, where the risk of this kind of situation is shared between contractor and client.

But while progress was made with instituting partnering in the early 2000s, much of this progress was ditched at the onset of recession in the face of the cheaper prices available to those clients going down the single-stage competitive tendering route. And in the face of Egan’s call in the nineties to innovate with modern methods of construction, the industry chose in large part to instead stick with its old ways, meeting demand by importing cheap skilled labour from Eastern Europe.

Yes, there are bright spots, such as the rise of BIM, and there is also a limited amount individual contractors struggling to keep their heads above water can do in the face of standard industry practice. But just a few weeks after the launch of a vision for construction in 2025, it is a bit deflating to realise how far the industry still has to go.

So far this housing recovery has yet to hit other sectors. The wider industry still has a chance to start investing enough in its staff, introducing innovation to how projects are delivered, and really committing to partnering to head off these problems. But it has been damaged by cut-throat competition in the recession and is still too often divided. The question is whether it is capable of overcoming these problems and grasping this opportunity.

Joey Gardiner, assistant editor

No comments yet