Prices have continued to stagnate in 2011, says Peter Fordham of Davis Langdon, an Aecom company. And with the eurozone crisis and global unease, construction isn’t going anywhere fast

01 / EXECUTIVE SUMMARY

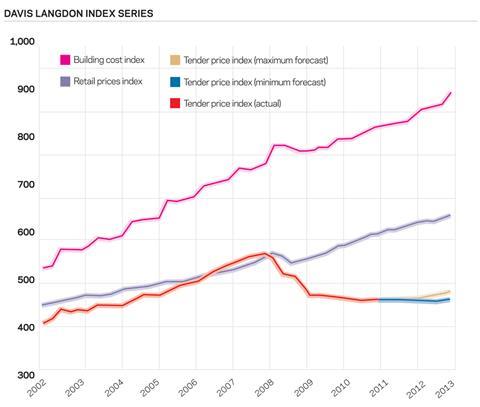

Tender price index

Tender prices are bumping along the bottom. Declining sentiment arising from financial markets’ uncertainty have reduced the outlook for recovery. Spare capacity in the industry will reduce the likelihood of short-term price rises in London and elsewhere.

�ڶ����� cost index

�ڶ����� costs rose 3.3% in the year to the third quarter 2011. Materials price inflation has eased over the last three months but the national wage agreement has brought in a small increase for building operatives for the first time in more than three years. �ڶ����� cost inflation over the year ahead is likely to be of similar magnitude.

Retail prices index

Retail price inflation rose to 5.6% in September, its highest rate for over 20 years. Consumer price inflation rose to 5.2% and has been at least double the government target of 2% all year.

The increases are largely due to sharp rises in gas and electricity bills. Inflation is unlikely to fall back to target before the end of 2012.

02 / TRENDS AND FORECAST

The construction industry appears to be “bumping along the bottom” as contractors - fearful of the future and aiming to cut costs to win work - contend with still-rising materials prices. Overall, prices in 2011 have been virtually flat. When able to, contractors have sought to recover increased costs but, more often than not, competition has prevented any meaningful increase in prices.

The governor of the Bank of England recently warned that the current financial crisis was “the worst since the thirties, if not ever” and the NIESR suggests that this recovery will be the weakest of any since the end of the First World War. The construction industry is bearing its fair share of the pain - new orders in the second quarter of this year were the lowest since records began in 1964. The private sector is not growing anywhere near as fast as the public sector is falling, reflected both in record unemployment figures and the collapsing level of new construction orders. Occupier demand is weak and development finance remains hard to come by.

With new orders dropping markedly (see page 48), contractors completing projects are anxious about where the next work will come from. �ڶ����� reported only recently (7 October) how some of the UK’s biggest contractors have embarked on a new round of redundancies and restructuring, hitting the north of England in particular, as the new North-South divide in construction opportunities opens wider. There are now a few extra tower cranes on the London skyline as some new projects got under way at the beginning of the year but in the North, such beasts are increasingly rare.

In London, there is still a very strong pipeline of new work that is primed to go to site during the first half of next year but it is clear that developers are anxious about the unfolding problems associated with the eurozone crisis and its effect on business confidence in general. As a result, the development process is slowing once again and development funding is ever more reliant on pre-lets. Occupiers are reviewing their property needs as more are shrinking than growing and existing tenants are being wooed by their landlords to stay with offers of lease extensions or other incentives. This may end up generating more refurbishment projects at the expense of new builds.

Increased materials costs continue to be an issue for contractors and this is reflected in some tenders. However, there is some evidence that site labour rates are still being trimmed to compensate. Preliminaries costs seem to have been cut as far as they can go and, while there are still examples of single-figure percentages, additions of 10-12% are perhaps the norm, as lower figures can barely cover minimal management requirements and health and safety issues. Specialist works packages such as IT, catering, bespoke joinery and lighting, for instance, have less room to manoeuvre and have seen some price increases this year. However, there are some signs now that materials price increases may be tempering, particularly following the recent commodity price “corrections”.

There is some evidence that risk is beginning to be viewed differently and some contractors and subcontractors are steering clear of suicide bids. But the norm remains that contractors continue to find further cuts, hoping to recover ground once the job is won. This leads to the continued fear of someone in the supply chain failing. Up to now, there have been fewer insolvencies than many predicted. The demise of Holloway White Allom at the beginning of the month was perhaps the largest casualty of the year so far. In Ireland a recent report from the Society of Chartered Surveyors showed that below-cost tenders were approximately 17% below realistic construction costs and that 55% of quantity surveyors had experience of projects failing to be completed because they were below cost.

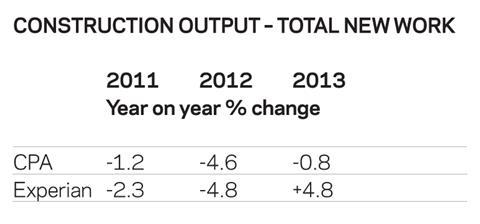

The short-term outlook for the industry is far from rosy. The latest new orders figures show that the volume of new work becoming available to contractors over the next few months will shrink sharply, further increasing competitive pressure for contractors seeking to replenish order books. Recently reviewed construction output forecasts by respected organisations such as the Construction Products Association (CPA) and Experian suggest at least another 18 months of increasing pain before any hope of improvement.

Both organisations expect a significant further decline in activity next year, but differ on likely conditions in 2013: Experian expects a bounce back as private commercial work recovers, aided by significant improvements in infrastructure and private housing spending. The CPA is less optimistic regarding the speed of recovery of the private commercial sector and the flow of infrastructure work, postponing any positive change in overall construction activity until 2014.

This means a continuing hard time for contractors and subcontractors, who will be competing for this falling volume of work. This will make any increase in prices difficult to force through. The speed of the global economic recovery may dictate how commodity prices fare: if the emerging economies continue to grow strongly, prices for commodities such as oil and steel may begin to rise again, in which case it may be impossible for some price rises not to pass through the supply chain. But competitive pressures will restrict any such price rises to the minimum.

The London construction market no longer looks bullish and any price movement over the next 12 months will be small. Prices could even fall further as prices for components like steel are currently slipping and the effect of the recent collapse in commodity prices takes the heat out of materials prices generally. Nevertheless, there is still expected to be an increase in construction activity in London over the next 12 months, so prices could move in the range of -0.5% to +1%.

The following year, so long as the economic turmoil is behind, further confidence should return, but as there are likely to be contractors that still have large pools of untapped capacity, price rises may still be restricted to 1-2.5%.

Contracting outside of London and the South-east looks set to be a testing occupation. Many of the regions will be disproportionately hit by the public sector cutbacks and the private sector has no appetite for development. It seems almost inevitable that prices in most regions have further to fall but the floor cannot be far away, so a price reduction of 1-2% over the next year should be anticipated but perhaps little or no change during the following year.

03 / HOT TOPIC – ECONOMIC CRISIS PART 2

The world - and Europe in particular - seems to be entering a period of near paralysis. The fear of Greece defaulting on its debt, causing untold damage to banks across the continent and possible contagion to other countries has made commerce stop in its tracks as if caught in headlights.

The IMF’s conclusion in its September Regional Economic Outlook: Europe was that European economies now face the prospect of a pronounced slowdown. In the UK, GDP increased by just 0.1% in the second quarter of 2011 and by 0.6% over the year. In March, the Office for Budget Responsibility forecast growth of 1.7% for 2011. The Ernst & Young Item Club now forecast growth of just 0.9% this year. Capital Economics have just issued a forecast of zero growth for 2012.

In the second quarter, output of production industries fell by 1.2% and household final consumption expenditure by 0.8%; the figure was saved by construction, which recorded an increase of 1.1% in output. GDP is unlikely to be saved by construction in the next few quarters.

The uncertainty in financial markets has caused both business and consumer confidence to drop. Hopes for an export-led recovery look ill founded as the UK’s major markets in Europe and the US are themselves retrenching. Exports from both manufacturing and service sectors have fallen to their lowest levels since 2009. Exports to major eurozone economies including Germany, France and Italy all fell in August, a decline expected to accelerate as demand falls across Europe.

The problems of a faltering recovery are displayed worldwide. Growth has decelerated in most major OECD economies. The OECD estimates that economic growth in the G7 economies excluding Japan will remain at an annualised rate of less than 1% in the second half of 2011. Their Composite Leading Indicators (CLI), designed to anticipate turning points in economic activity relative to trend, continue to point to a slowdown in economic activity in most OECD countries. The CLI for the OECD area fell in August for the sixth consecutive month. The CLI for the UK fell for the seventh consecutive month and is now below 100, pointing strongly to a slowdown in economic activity below long-term trend.

It is feared that the current market turmoil could lead to a tightening in credit conditions. The last Bank of England Credit Condition Survey showed credit conditions relatively unchanged for most corporates but reduced availability in the commercial real estate sector, perceived as higher risk. Lenders pointed to adverse wholesale funding conditions, which might constrain future lending while demand for credit was also expected to fall in the coming three months.

Deteriorating business indicators eventually persuaded the Bank of England to embark on another round of quantitative easing, lifting the asset purchase programme a further £75bn to £275bn. Recent analysis by the Bank of England suggests that the £200bn of assets purchased between March 2009 and January 2010 boosted GDP by between 1.5% and 2%. However, the UK seems intent on ignoring the IMF’s warning against imposing budget cuts at the expense of growth. While Europe flounders and the UK sinks, will there be a Plan B?

04 / ACTIVITY INDICATORS

Office for National Statistics

Official figures for construction output show activity holding up well. Figures for the three months to August show that construction output at constant seasonally adjusted prices fell 2% compared with the previous three months. However, for the year to date the volume of construction output is 2% higher than during the corresponding period last year. Housing, in particular, has fared well, increasing its volume nationally by 8%.

By contrast, the figures for new orders paint a very bleak picture. The volume of new orders in the first quarter (at constant prices) was 10% down on the average quarterly figure for 2010. The volume of new orders in the second quarter fell another 16%, potentially shrinking the future size of the industry by more than a quarter. The value of new orders in the second quarter was the lowest since this series of data began in 1964.

Unsurprisingly, new orders in the public sector have been severely damaged by the government’s austerity measures. Orders in the second quarter, following the start of the new financial year, were just 60% of the average quarterly value last year. At current prices, almost £1.2bn per quarter has been removed from the industry.

Infrastructure has been similarly hit. Here the value of orders in the second quarter were worth little more than 50% of last year’s quarterly average value. Spending on railways has actually increased but new work ordered on water, electricity and roads represents less than half of last year’s commitment.

Markt/CIPS UK Construction PMI

The latest Purchasing Managers’ Index suggests that the level of activity in UK construction is flat after recording some small level of increase every month during 2011. However, both housing and civil engineering activity was down, while commercial activity increased.

The survey confirmed the Office for National Statistics data in recording a reduction in new orders, although this was the first such observation since February 2010. The survey also picked up that some projects were once again being delayed or cancelled as a result of weak client confidence.

Experian Construction Industry Focus

The Experian survey (reported in ) also recorded a level of no change in August, although it was the residential sector that showed growth while non-residential work and civil engineering continued to decline. Scotland remains the brightest area while contractors in the North-west continue to be the most despondent.

FMB State of Trade Survey

The FMB’s Q3 2011 survey found that workloads for small and medium-sized contractors decreased for the fifteenth consecutive quarter since the recession began in Q1 2008. The level of enquiries worsened, supporting the data above, and further drops in workload are anticipated for the rest of this year across all sectors.

05 / BUILDING COST INDEX

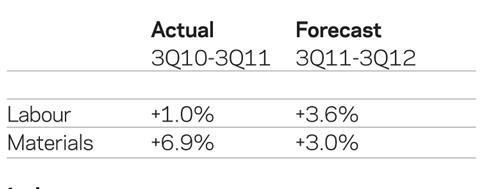

The �ڶ����� Cost Index rose by 0.7% in the third quarter 2011 and is 3.3% higher over the year, dominated by rising materials prices. Over the year ahead the index is forecast to rise by a similar amount but with lower materials price inflation and labour costs beginning to have an influence for the first time in almost three years.

Labour

Minimum pay rates for building and civil engineering operatives rose by 1.5% from 5 September after a three-year pay freeze. Employers had been trying to hold out until 2012 but gave in to this compromise deal. Talks are planned to begin early in 2012 for a further deal next year.

Conditions are unlikely to exist to enable the employers to offer a substantial further deal but costs will also be increased by having to fund the additional bank holiday for the Queen’s jubilee next year.

Meanwhile, wage rates for electricians and heating and ventilating operatives remain frozen. A number of major services engineering companies are trying to withdraw from the existing national wage agreements and introduce a new agreement that will see the greater use of semi-skilled grades, which the unions insist is a way of deskilling the industry and lowering pay.

Official figures show that average earnings in the construction industry in the three months to August were 2.2% higher than a year before, the highest figure for 17 months and having been negative from August 2010 to May 2011. Site rates, including self-employed and agency workers, however, have fallen further over the last year.

Materials

Figures from the Office for National Statistics show that construction materials prices stabilised in the three months to August but were still 6.9% higher than a year before after reaching an annual inflation figure of 9.1% in March.

Reinforcement prices have topped the list of materials price increases for some time. Prices in August were 16% higher than a year before, following a surge at the beginning of the year, driven by higher world scrap prices. Scrap prices have been relatively stable in 2011 but are likely to soften in the short term as demand from steel manufacturers eases in response to lower output. Reinforcement prices are expected to trend downwards for the remainder of this year as demand remains weak.

Many construction materials prices are subject to the vagaries of the world commodities markets, where prices have seen a steady recovery from their collapse in 2008, but May brought a reversal as renewed concerns about global recovery took hold. Recent weeks have witnessed volatility in the commodities markets as prices have responded to rapidly changing political and economic conditions. Overall, oil and metals prices have fallen 13% and 10% respectively since May. Global steel prices have fallen by 7% but remain 14% higher over the year.

Tata Steel increased prices for structural sections by £50 per tonne at the beginning of September, in line with other European suppliers, blaming increases in raw material costs in the first half of 2011. Those higher prices for iron ore, coal and scrap have largely held up but weak demand brings into question steel manufacturers’ ability to reap the benefits of higher list prices at the same time as some introduce production cuts.

The biggest “casualty” from the recent commodities price fall-out has been copper. Prices fell by 30% from the level just below $10,000 (£6,334) a tonne at the beginning of August to below $7,000 (£4,438) a tonne at the beginning of October. Some recovery has seen the cash price climb to $7,500 (£4,755) a tonne, still its lowest price for more than a year. As a result some of the cost pressures faced by electrical component manufacturers will have eased.

No comments yet