Last week, Interserve outlined its latest rescue plan to try to halt the slide that has seen market value collapse in the past two years. But with its largest shareholder planning to revolt against the deal, what hope is there that the business will survive?

Ten minutes after announcing details of its latest rescue plan last Wednesday morning, Interserve was forced to put out another update telling the market that a New York-based hedge fund called Coltrane Asset Management, which has a 17% stake in the business, was intending to organise a shareholder revolt against the plan.

Coltrane, which made millions of pounds betting on the demise of InterserveŌĆÖs rival contractor Carillion last year, wants to vote out all of the groupŌĆÖs board with the exception of chief executive Debbie White and is hoping to persuade other shareholders to take up the fight. In short, the rescue plan will see InterserveŌĆÖs lenders cut what theyŌĆÖre owed by half, swapping their stakes for shares, resulting in creditors owning 97.5% of the company. Unsurprisingly, Coltrane isnŌĆÖt too keen to see its stake wiped out like this and has requisitioned an extraordinary general meeting to be held by the end of March.

Among those it wants gone are chairman Glyn Barker, chief financial officer Mark Whiteling and non-executive Nick Pollard, the former Balfour Beatty, Skanska and Bovis Lend Lease executive who joined last June and who, as the boss of Cory Riverside Energy, an energy-from-waste firm, has been helping try to find the best way out of InterserveŌĆÖs disastrous EfW contracts.

Interserve announced this morning that another name on its hit list, Dougie Sutherland, the main board director in charge of sorting out its problem energy-from-waste (EfW) jobs, had stepped down with immediate effect and was formally leaving the firm at the end of the month, ending a 12 year association with the business.

ŌĆ£There could be a sufficient number of unhappy existing holders disenchanted enough to write off the balance of their massively diluted investmentsŌĆØ

Kevin Cammack, Cenkos

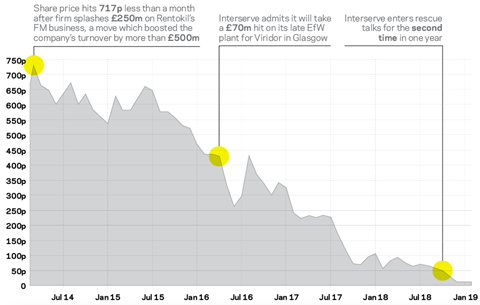

A timeline of InterserveŌĆÖs financial problems - keep up to date

Coltrane would prefer to see an alternative recovery plan, which would safeguard shareholder value and work down debt more slowly through cash generation along with the odd disposal here and there, rather than hand control of the business to banks such as HSBC, BNP Paribas and Royal Bank of Scotland which, along with other lenders, have agreed to cut net debt to ┬Ż275m in exchange for ┬Ż480m of new shares. Existing lenders will also provide an extra ┬Ż75m in liquidity.

Cenkos analyst Kevin Cammack thinks Coltrane might have a chance of pulling off a revolt. ŌĆ£There could be a sufficient number of unhappy existing holders disenchanted enough to write off the balance of their massively diluted investments rather than see the business effectively passed into the hands of its lenders.ŌĆØ

And a source close to Coltrane said: ŌĆ£Shareholders will be wiped out by this restructuring. ItŌĆÖs difficult to see shareholders not agreeing with what Coltrane is saying.ŌĆØ

But White has said the plan, which has the backing of the government, is pretty much the only deal available. ŌĆ£The board believes that this agreement will secure a strong future for Interserve,ŌĆØ she said when the rescue plan was announced. ŌĆ£Its successful implementation is critical to the Interserve groupŌĆÖs future and all of its stakeholders.ŌĆØ

Any shareholder revolt, though, could prove to be just a ŌĆ£damn youŌĆØ one, an empty protest with no real alternative to support it. But what happens if shareholders do vote it down when it is finally stitched together and presented to shareholders in the next few weeks?

ŌĆ£Two weeks ago, I would have said it was 95% they will go. Now IŌĆÖd say itŌĆÖs more like 60:40 they will surviveŌĆØ

Tony Williams, ║┌Č┤╔ńŪ° Value

Cammack says an obvious lack of an alternative might be enough to convince shareholders to back it, however reluctantly. ŌĆ£Of course, dilution to just 2.5% of the enlarged equity is a hard pill to swallow but at least it is 2.5% of something rather than 100% of nothing.ŌĆØ And he adds: ŌĆ£Just what is [plan B] beyond turning to government for financial support ŌĆō or begging?ŌĆØ The alternative, some people believe, is the risk that Interserve will fall into administration.

InterserveŌĆÖs most successful business, the RMD Kwikform shoring subsidiary, is being kept in the company, after the Cabinet Office spiked plans by the banks to spin it off because of concerns that without RMD, which in 2017 made a pre-tax profit of ┬Ż15m from a ┬Ż42m turnover, Interserve would be too weak to be awarded government contracts which account for around 70% of the firmŌĆÖs ┬Ż3.7bn turnover. Instead, the price RMD will have to pay is having around ┬Ż350m of existing debt allocated to it over the next four-and-a-bit years.

Cammack, who 18 months ago called for Interserve to hoist the ŌĆ£for saleŌĆØ sign over RMD in the hope of picking up ┬Ż200m for the business, says RMD ŌĆ£will need every day of the four- to five-year term to make any sort of inroads into the [debt which] also reduces its [RMDŌĆÖs] saleabilityŌĆØ.

WhatŌĆÖs happened since the last rescue deal

March 2018: Interserve agrees ┬Ż300m rescue deal with lenders

April: Interserve announces ┬Ż244m pre-tax loss for 2017 with net debt at year-end standing at ┬Ż503m

August: Interserve says cost of energy-from-waste has gone up to ┬Ż227m. Net debt at half-year to 30 June hits ┬Ż614m

November: Interserve misses deadline for handing over Derby energy-from-waste plant, helping send shares to a 34-year low. Government confirms it has asked Interserve to draw up ŌĆ£living willŌĆØ in case it goes bust. Firm says year-end net debt will be between ┬Ż625m and ┬Ż650m

December: Interserve share price drops to 6p as details emerge of second rescue deal. Executive board members Robin OŌĆÖKelly and Yvonne Thomas leave

January 2019: Hands over first of four energy-from-waste plants. Dunbar plant was due to be completed at the end of 2017

Energy from waste ŌĆō the capability gap

RMD was being readied for sale three years ago, with InterserveŌĆÖs then chief executive Adrian Ringrose saying it had put the business under a strategic review when announcing its 2015 results in February 2016. But eight months later RMD was told it would be staying at Interserve. Four weeks after that, Ringrose was off ŌĆō with Interserve telling the market the man who had masterminded its disastrous foray into the EfW sector would be leaving the following year.

Energy-from-waste has been the running sore that has provided the backdrop to the firmŌĆÖs problems for some time now. Gordon Kew, InterserveŌĆÖs former boss of its construction business, admitted to ║┌Č┤╔ńŪ° last May that the firm had woefully underestimated the EfW market. ŌĆ£There was definitely a capability gap,ŌĆØ Kew admitted. ŌĆ£We went into a new sector that weŌĆÖd thought weŌĆÖd prepared for and clearly we hadnŌĆÖt.ŌĆØ

Kew has since moved on, leaving the business last September as part of WhiteŌĆÖs streamlining process, joining ISG last month as its chief operating officer. While still at Interserve, he said the business expected to have wrapped up completing its EfW work by the end of last year. It proved to be another EfW deadline missed and the firm still needs to complete three more EfW plants after handing over a plant in Dunbar, Scotland, last month to client Viridor ŌĆō the same one that kicked Interserve off a similar job in Glasgow back in autumn 2016 and which claims the firm owes it more than ┬Ż60m.

The remaining jobs are in joint venture with US energy tech firm Babcock & Wilcox in Rotherham, South Yorkshire, and Margam in south Wales ŌĆō as well as a plant in Derby being developed with waste management specialist Renewi. Babcock & Wilcox has previously told investors that each of the three plants it was building in the UK, including Dunbar, would be finished by this July.

The whole EfW misstep, which began nearly seven years ago when the firm won a ┬Ż146m deal to build a new facility in Glasgow, has cost the business more than ┬Ż220m. Speaking to ║┌Č┤╔ńŪ° 15 months ago, before he joined Interserve as a non-executive director, Pollard was damning of firms like Interserve which went into a market they are unfamiliar with. ŌĆ£If you donŌĆÖt understand the risk or donŌĆÖt have the people to construct that asset, donŌĆÖt do it.ŌĆØ

Avoiding another Carillion

Interserve has not yet said when it will publish its 2018 results, but if last year is anything to go by ŌĆō when it filed on the last possible day it could ŌĆō we might have to wait until the end of April. ItŌĆÖs unlikely to put any numbers out until full details of the deleveraging plan are out and signed off by shareholders. The firm, which last published a trading update on 23 November last year, has a market cap of ┬Ż17m ŌĆō down from ┬Ż500m two years ago ŌĆō so the cynics will point out thereŌĆÖs not much further for it to fall in that regard.

But local councils have their worries and have been drawing up contingency plans in case it does ŌĆō such is their fear of being landed with a Carillion-style hit on local services.

Interserve has been on the Cabinet OfficeŌĆÖs watch list of ŌĆ£at riskŌĆØ businesses, being required to draw up a so-called living will in the event of its collapse. And here is the major stumbling block for a Coltrane-led revolt. The government does not want another Carillion on its watch. Equally, it does not want to be pumping money into having to bail out a private firm that has run aground because of poor decision-making. ŌĆ£I suspect [InterserveŌĆÖs plan] will prove to be the best deal in town,ŌĆØ says Cammack. ŌĆ£This was never going to be easy and anything other than painful for investors.ŌĆØ

Tony Williams, an analyst at ║┌Č┤╔ńŪ° Value, says Interserve is clinging on by its fingernails but has a better chance of survival than it did before. ŌĆ£Two weeks ago, I would have said it was 95% they will go. Now IŌĆÖd say itŌĆÖs more like 60:40 they will survive. There is a business still there and if it can bump along the bottom, then it could recover. Costain went down to a penny stock [back in the 1990s] and recovered with the help of overseas investors.ŌĆØ

But do the brightest and the best want to work there? Williams thinks Interserve will have to pay top dollar to attract and retain people, but already some have decided enough is enough. Matthew Fundrey, the bid director at InterserveŌĆÖs Paragon fit-out business, has joined Mace. Williams thinks that up to 10% of InterserveŌĆÖs 75,000 staff worldwide ŌĆō 45,000 of them in the UK ŌĆō could eventually be eased out as part of any recovery strategy.

At best, the plan announced last week would seem to represent the least-worst option for a business that saw its shares sink to their lowest amount since 1984 last November, only for them to slide even further the following month, at one point dropping to 6.5p on 10 December, as investors digested the initial reports of what sort of haircut they were going to have to take on their stakes. Under this plan, the government doesnŌĆÖt lose money and another construction firm doesnŌĆÖt go under.

Still, investors would do well to avoid casting their minds back to the peak days of 2014. Then, InterserveŌĆÖs shares traded for 717p each.

No comments yet