The trend continues for rising optimism and workload, though materials costs and wage rates are also increasing, while market uncertainty may have some surprises to pull, says Michael Hubbard of Aecom

01 / Executive summary

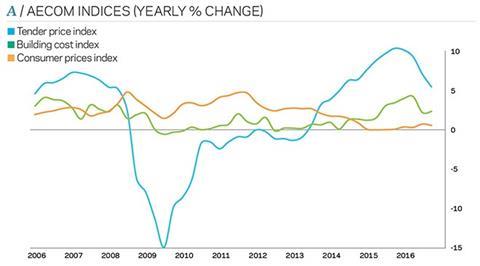

Tender price index ▲

Tender prices increased in Q4 2016 by 5.5% provisionally compared with the same time a year earlier. More upside risks to the outlook are expected through 2017 than last time.

�ڶ����� cost index ▲

�ڶ����� materials cost inflation continues to pick up pace, increasing by an average of 2.5% from Q4 2016 to Q1 2017 – an equivalent annualised basis of 10%.

Retail prices index ▲

The annual rate of change was 2.1% in Q4 2016. Domestic inflationary pressures continue to rise.

02 / Trends and forecasts

New year, old trends – “old” in that they are well established over the last few years. Early 2017 is expected to see more of the same for the construction sector: capacity constraints, good workload, increasing labour wage rates and overall optimism. Added to this are rising materials costs, primarily driven by the significant changes to sterling exchange rates. Yet more organisations are beginning to wonder what the future holds.

Against this backdrop, uncertainty and tension remains with respect to geopolitical issues and the UK’s position in the world. A steady stream of rolling speculation, with occasional news thrown in, does not quell the level of uncertainty. But many are still left wondering if Brexit really is a tipping point. Certainly, it is not without consequences. Political risks are beginning to be addressed with early announcements on what place the UK will seek in the world economy and what the country leaving the European Union will mean. As the UK government indicates its intentions and what place it intends to try to negotiate for itself with its neighbours and the world, then investment decisions affecting construction output over the medium-term will become clearer. Or, at the very least, it will provide some context and perhaps greater clarity in which decisions can be made.

Although the Autumn Statement underwhelmed with its immediate benefits to construction sector output from fiscal stimulus, longer-term policies introduced post-Brexit to address productivity issues in the UK ought to bring major benefits for construction and infrastructure output. Public and regulated sector projects and programmes do feature on the radars of main contractors. A definite shift among contractors towards balancing portfolios has taken place over recent years – and continues to do so – with an expectation that public and regulated sector work will insulate against any private sector workload chills in the future. Resilience is the watchword here.

Balancing risk and reward remains a central goal of main contractors and supply chain firms. The intention is that it leads to organic or sustainable ways of filling order books. This includes concentrating on those sectors deemed to be core to business planning, seeking work from repeat customers and being a contractor of choice for clients where negotiated procurement plays a greater role. Additionally, balanced risk and reward also extends to procurement routes and the level of bidding competition – in other words, how many and which competitors are on the tender list.

Meanwhile, tendering costs are considerable. Aligning bidding and project delivery resources to projects that enable the best chance of success are vital to the overall selection process. This factor, in conjunction with operational cost efficiency, results in main contractors often choosing to allocate bid resources to those projects deemed winnable and, if successfully delivered, will return margin targets. In some instances – and what was usually seen among larger contractors but which is also evident among mid-size contractors now – is further segregation of the supply chain as some main contractors are unwilling to be on a tender list unless up against similar sized firms.

Although pinch points in the supply chain still exist, response times to client-initiated enquiries have shortened in some instances along with a greater willingness to discuss a project. Yet some trades are still declining to submit bids, mostly because of resource availability. Early supply chain involvement, and procurement routes that promote this, can help to generate interest in a project and allow management of available capacity. Methods of risk mitigation are also seeing focus in order to hit tougher budgetary constraints of clients.

External factors are critical too. Time is often spent assessing the client’s cost and programme expectations – or the apparent robustness of these – to assess likelihood of success and the chance of the project going ahead. Market conditions have meant – and continue to mean – that governance plays a central role in not buying projects that might lead to problems. After all, you can always recover from the project you didn’t win; you may never recover from the project won at the wrong price.

Many contractors are confident that this year’s pipelines of work are well on the way to being secured, despite some reductions in enquiries and tendering activity following the EU referendum. The immediate period after the Brexit vote saw some projects pause. Many are now live again. Enquiries from multi-national companies looking at European locations have increased, though, most likely arising from strategic and contingency planning.

An optimistic outlook remains the predominant view across the industry at this point in time, as project restarts and existing momentum provide weight to the belief that 2017 will post good levels of industry output. Upward revised UK economic growth forecasts help here too. A downside risk to this is that some clients are responding to prevailing ambiguity by considering phasing their future programmes and projects to reduce or minimise exposure to external events and trends.

Selectivity has been a constant throughout 2016 and will endure into 2017 for many trades. However, where all contractors and trades were able to pick and choose their work over the last two years, changes to this total number are emerging. Future projects are being brought to market and often the onus still remains on clients to sell their projects to main contractors that remain bullish on secured work. The 2017 pipelines are strong, with 2018 also looking reasonably healthy at the early stages of this new year. Nevertheless, a transition period will begin in 2017 where sellers of building and construction services who still need to secure workload for 2018 converge with buyers holding constrained budgets. Deals will be done but with different commercial terms to those of recent years.

03 / Activity indicators

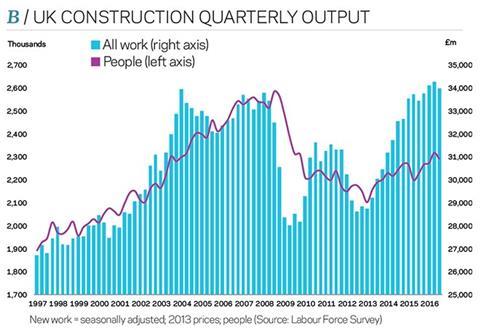

All work construction output carried forward the broadly flat, yet positive, yearly growth trend through 2016 into its final quarter. Office for National Statistics (ONS) construction output data recorded a modest increase of 1.5% in November compared with the same month a year earlier. All new work increased by 4.4% – the fly in the ointment was this being offset by a 4% drop year-on-year in repair and maintenance work, which accounts for about 35% of all industry output.

Looking across the sector breakdown, private housing work remains the engine of construction industry new workload. Notably, this was joined by a sizeable yearly percentage change to public sector housing work. Some words of caution, though, on this data point: the public sector yearly percentage change is due to denominator effects of the preceding year; and the sector’s output is comparatively small. Two of the three largest sectors in absolute numbers – private housing and commercial – are where yearly growth is unequivocally clear. But for these sectors, overall output looks very different indeed.

Anecdotally, main contractor confidence on 2017 order books, and increasingly on 2018, is evident. There is a feeling that sufficient opportunities exist to secure workload for 2018. Trade contractors mirror this sentiment in the main, with some maintaining they have full order books for 2017 and are only after opportunities that deliver turnover in 2018.

A quarter of main contractors were unable to bid for opportunities because of labour shortages according to Build UK’s state of trade survey published towards the end of last year. This is compounded by the fact that labour costs are rising still. Both technical and trade staff are in demand. Further, this survey and others highlighted that capacity continued to tighten over the second half of 2016. When considering this over the longer term, it highlights the need to retain and train staff in order to meet longer-term business objectives. Although flatter output growth is forecast, paradoxically this may have benefits for businesses in there being a steadier state and therefore more stability for future planning.

Economic indicators and business sentiment surveys have all posted robust levels in recent months. Although consumer confidence took a slight dip towards the end of the year, there remains momentum in economic activity. However, investment intentions are more muted, reflecting the medium to longer-term uncertainties generally.

Growth rates are different for the various UK economic sectors: consumer-facing industries faring significantly better on a comparative basis than the production, manufacturing and construction industries. Again, this underlines the persistent imbalances to the UK economy.

The Confederation of British Industry’s Industrial Trends Orders posted a strong data point in January. This survey measures the expectations of manufacturing businesses, providing a good litmus test to prevailing economic conditions. Sterling depreciation has played a role here.

Construction-specific surveys support these favourable broader indicators too. The RICS and the Federation of Master Builders’ surveys highlighted again the skills shortages in the industry for both trades and technical skills.

Both surveys indicated positive views on sentiment and future workload improvements. Encouraging present activity levels also came through in the CIPS Markit construction PMI, despite a slight fall from 54.2 to 52.2 in January but remaining close to its long-run average.

04 / �ڶ����� costs and prices

Construction prices rose over the year at Q4 2016 by 5.5% according to Aecom’s tender price index, which uses Greater London as a base location. Although now slowing, this yearly rate of change maintains a level that is higher than long-run averages for tender price inflation and pushes the index level to new highs. Slower rates of yearly change are expected over the next 24 months.

Although uncertainty has increased throughout the industry, its effects on market pricing have so far been muted. Nonetheless, lower expected output will add increasingly greater pressure for the need to adjust price trends – slower or lower than recent trends is then the order of the day for pricing, in order to maintain a competitive edge.

Meanwhile, price levels are experiencing growing pressure from rising input costs. Input costs generally for all industries are rising at their fastest rate since 2008, according to the government’s producer price inflation indices. These measure the price changes of goods bought and sold by UK manufacturers.

�ڶ����� materials have also seen notable changes over the latter quarters of 2016 to previous benign inflation trends. The average increase in materials prices from Q4 2016 to Q1 2017 was 2.5% (equivalent to 10% currently on an annualised basis). There was a larger increase in metal items, which tend to be imported in the main. Significantly, there were no price reductions in any materials groups over the period.

Domestic inflation is also adding to the build-up of pressure in the construction value chain and pricing. While the pass-through of price adjustments arising from the devaluation of sterling is becoming more common, it is still not wholesale. That said, if sterling remains weaker for an extended period of time, then the inevitability of price increases becomes greater, and with higher rates of domestic inflation too.

Construction labour rates continue to rise on a yearly basis. This adds additional pricing pressure for the supply chain. Add to this a good dose of bullishness on secured short and medium-term workload and there are fewer reasons not to pass on these rising input costs at the moment. Greater uncertainty over the medium-term will change this view, however. Further complications may arise from Brexit negotiations and labour restrictions.

As general inflation in the UK accelerates, this adds to the probability of more construction wage growth over the year. Commodity prices are also rising, with forecasts of more increases through 2017.

The World Bank’s latest forecasts suggest upwards of 10% increases set for this year. Last year’s advances were driven to a large extent by Chinese demand from fiscal stimulus. Recent views on the rally for iron ore are that it is now more speculative in nature and that 2017 will see more supply to the market. This should therefore lower prices for iron ore. However, if new US policies for growth act as a demand stimulus, particularly for infrastructure works, and combined with renewed fiscal growth policies in China, then iron ore prices at the least will see a floor.

There are the first signs that main contractor preliminaries costs are being adjusted. Indirect costs have steadily increased for the last few years, so too unit rates. Now though, there are the first signs of a break in this trend for preliminaries. While this is not across the board, and depends to a large degree on the project parameters, this is a likely response to industry output changes, lingering uncertainty for the medium-term and the need to retain a competitive edge. Interestingly, these emerging adjustments to prelims are happening when unit rates are still rising across most direct cost items. This highlights the overwhelming influence of supply chain costs on overall price levels.

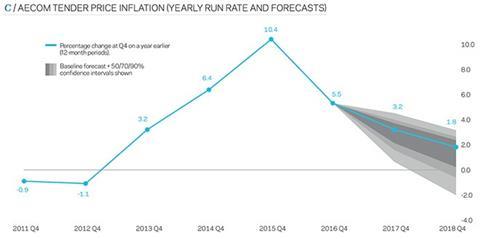

Aecom’s baseline forecasts for tender price inflation are 3.2% from Q4 2016 to Q4 2017, and 1.8% from Q4 2017 to Q4 2018. Upside risks to pricing have increased since last time, reflecting the evident – and growing – pressures from domestic inflation, and that industry output has not followed the path of pessimistic near-term forecasts post-EU referendum. Downside risks are still evident, with a higher probability for these to affect pricing across the latter forecast period.

The price forecasts are based on a number of key assumptions: construction output continues a planar trend; Brexit-related events in the short-term continue to ignore the more pessimistic forecasts of an immediate and sustained downturn, but over the medium-term risks do weigh to the downside; order books remain firm but uncertainty begins to increase in the second half of 2017 and into 2018; prevailing trends in government capital expenditure are not substantially changed in the short term; and sterling strengthens moderately.

No comments yet