Little growth was in evidence as most indices stayed steady or contracted, while all sectors experienced less work in hand. However, labour shortages have eased since last summer. Experian Economics reports

01 / State of play

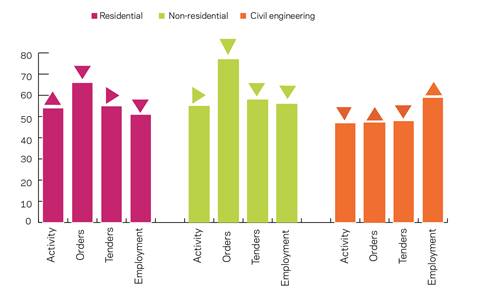

The total activity index gained one point from November and reached 55, reversing the negative trend of the previous three months. The repair and maintenance index stood at 57, two points down from November, but still considerably above the average value of 50 for 2017.

The residential and non-residential activity indices were in positive territory, whereas the civil engineering index moved into contraction. The residential activity index increased by three points to 54, while December’s non-residential activity index remained at 55. The civil engineering index lost six points to 47 and fell below the threshold of 50, indicating falling activity.

Both orders and tender enquiries lost points in December, although still showing growth; the growth in orders was faster than the growth in tender enquiries at 65 and 56 respectively.

On a sectoral basis, the civil engineering orders index was the only one showing growth – of three points to 47 – although this still left it below normal for the time of year. The residential orders index dropped by three points and the non-residential orders index fell by two points, but both remained above normal.

Tender enquiries showed no growth in their respective indices. The residential index remained at 55, whereas non-residential was two points down to 58 and civil engineering took a 15-point slump into negative territory at 48.

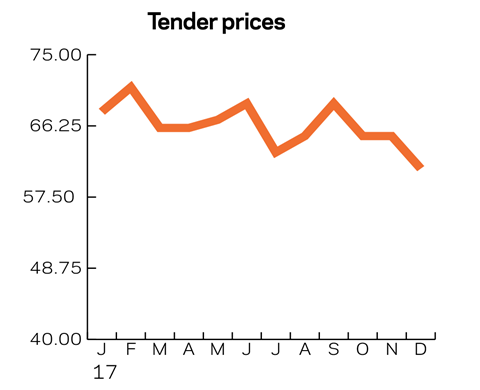

The tender prices index lost four points to 61, the lowest value since July 2016. The employment prospects index continued losing ground and reached 53, four points down from November.

Labour shortages were reported as a constraint by 10% of respondents, about one percentage point less than the previous month. The share of respondents reporting labour shortages has eased in the second half of 2017, from a peak of 20% in July, which chimes with the falling output profile reported by the Office for National Statistics.

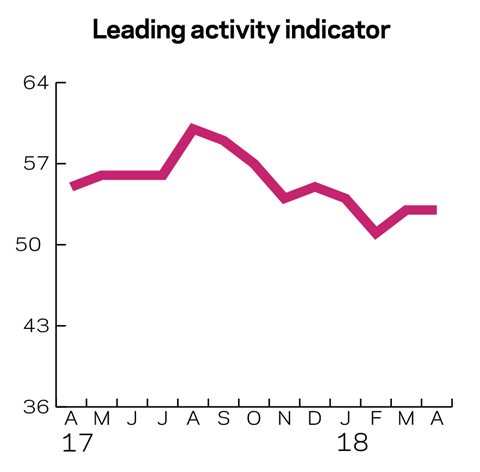

02 / Leading construction activity indicators

The contractors’ activity index stood at 55 points in December 2017, indicating expansion. The figure was one point above the previous month’s results and at the average for 2017. The leading activity indicator is expected to stay above the no-growth threshold of 50; however, it is projected to decrease by a couple of points.

03 / Work in hand

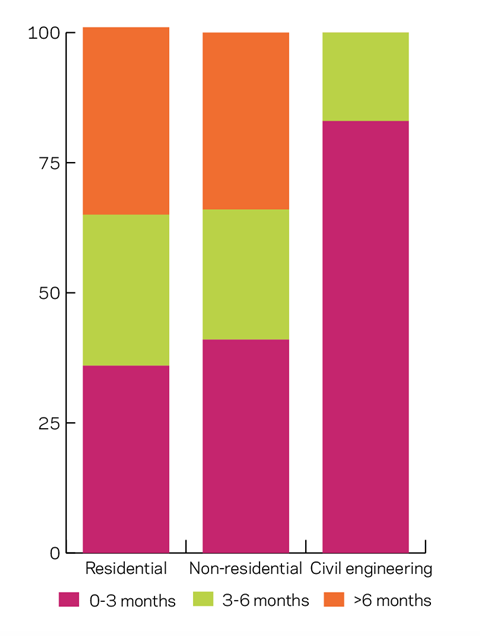

In the residential sector, the work in hand figures show a decrease. Since June 2017 the share of respondents with less than three months of work has been increasing and reached 36%. The share of respondents with three to six months’ work in hand also increased compared with September. These movements were apparently at the expense of respondents with more than six months’ work, whose share decreased by 18 percentage points.

The non-residential sector showed similar movements, albeit less pronounced. Respondents indicated having less work in hand compared with September 2017, with the percentage having less than six months’ work increasing somewhat.

The level of work in hand in the civil engineering sector has changed little in the past six months, although it is still following the trends in the other two sectors. The latest results show a slight increase in the share of respondents with work in hand of less than three months (three percentage points). Again, no respondents indicated more than six months of work in hand.

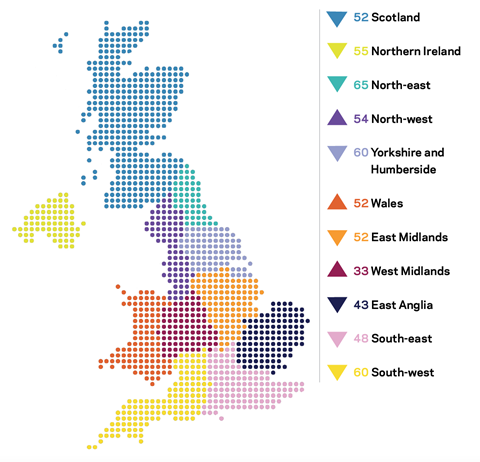

04 / Regional perspectives

Experian’s regional composite indices incorporate current activity levels, the state of order books and the level of tender enquiries received by contractors to provide a measure of the relative strength of each regional industry.

In December, eight of the regions expanded but only three saw their growth rate accelerate. Two regions, the South-east and East Anglia, entered negative territory. The former saw its index drop eight points to 48, and the latter seven points to 43.

Conversely, the North-west and Wales indices moved into positive territory. The North-west saw its index grow by five points to 54, partially reversing the contraction in the last two months. Wales recorded its first month of growth since April.

The best-performing regions – Yorkshire and the North-east – dropped by 17 and eight points respectively to 60 and 65. Therefore, all the regional indices were below 70 points in December.

The West Midlands continued to be the worst-performing region, with its seventh consecutive month of contraction, despite gaining one point.

The UK composite index fell by three points to 60, the third consecutive month of slowing growth. Despite the lost ground, the index is still comfortably in expansion territory.

This an extract from the monthly Focus survey of construction activity undertaken by Experian Economics on behalf of the European Commission as part of its suite of harmonised EU business surveys.

The full survey results and further information on Experian Economics’ forecasts and services can be obtained by calling 0207-746 8217 or logging on to

The survey is conducted monthly among 800 firms throughout the UK and the analysis is broken down by size of firm, sector of the industry and region. The results are weighted to reflect the size of respondents. As well as the results published in this extract, all of the monthly topics are available by sector, region and size of firm. In addition, quarterly questions seek information on materials costs, labour costs and work-in-hand.

No comments yet