Our quarterly analysis of costs and prices reveals an industry hit by wage agreement troubles and high input costs

1. Key changes

- �ڶ����� costs are pulled in different directions, with labour rates frozen and materials prices rising rapidly

- Consumer price inflation is at twice target and forecast to go higher before heading back towards target in 2012

- Manufacturing input costs are at heady levels but output prices are unable to match them

- Steel prices are pushing construction prices back towards double-digit inflation

- More wage agreements are frozen; builders await a possible new settlement

- Construction earnings are still falling but redundancies are declining.

Percentage change year-on-year (Q1 2010 to Q1 2011) : % Direction

- �ڶ����� cost index : 3.5

- Mechanical cost index : 4.2

- Electrical cost index : 2.2

- Consumer prices index : 4.2

(First quarter 2011 figures are provisional)

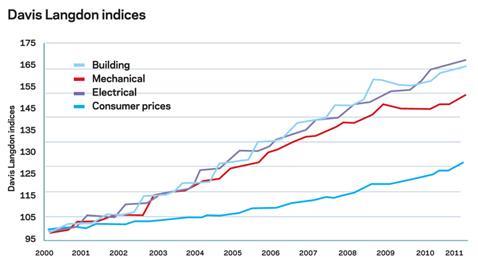

The following chart shows how Davis Langdon’s index series, reflecting cost movements in different sectors of the construction industry, have fared since 2000, with the movement of the consumer prices index for comparison.

�ڶ����� cost index

Inflation in the building cost index remains below its long-term average because wage rates remain frozen. However, materials prices surged again at the beginning of 2011, sending the index upwards.

Mechanical cost index

Inflation in the mechanical cost index is now back to its average level for the last decade and has been on an upward trend for five quarters, fuelled most recently by a sharp rise in materials prices since the beginning of the year.

Electrical cost index

Electrical materials price inflation remains close to 10% but, with labour rates frozen, year-on-year inflation is at its lowest level since 1999.

Consumer prices index

The consumer prices index remains at more than double the government’s target and is forecast to climb further before heading back towards target

in 2012.

2. Price adjustment formulae for construction contracts

Price adjustment formulae indices, compiled by the �ڶ����� Cost Information Service, are designed for the calculation of increased costs on fluctuating or variation of price contracts. They provide useful guidance on cost changes in various trades and industry sectors and on the differential movement of work sections in Spon’s Price Books.

Over the last 12 months between May 2010 and May 2011, the 60 building work categories have recorded an average rise of 4%, a decrease from 4.5% three months ago.

The largest price increases over the last year have been:

May 2010 - May 2011: % change

- Piling: steel : 14.6

- Pipes and accessories: aluminium : 12.2

- Cladding and covering: copper : 12.1

- Pipes and accessories: copper : 10.2

- Cladding and covering: lead : 9.9

- Pipes and accessories: steel : 9.8

- Concrete: reinforcement : 8.6

- Waterproofing: asphalt : 8.1

- Metal: miscellaneous : 7.9

- Pipes and accessories: Spun and cast iron : 7.5

Steel and metals are the common feature of the work categories above that have seen the largest cost increase over the last year. Steel prices rose again at the beginning of the year as manufacturers reacted to raw material price rises. Copper prices rose by two-thirds in the second half of 2010 but have been in decline since February.

Some of the more traditional trades have seen little or no cost movement over the last year:

May 2010-May 2011 : % change

- Brickwork and blockwork : 0.4

- Pipes and accessories: clay and concrete : 0.4

- Glazing : 0.0

- Finishes: screeds : 0.0

- Concrete: insitu : -0.5

Materials: Inflation soars and input costs rise, while output prices are struggling to stay on track

3. Executive summary

- Consumer price inflation continues way above target and may rise further before falling back

- Industries’ input costs are heading back to record levels, driven by oil prices

- Industries’ output prices are struggling to maintain track in the current economic climate

- Metals prices are down from recent peaks

- Construction materials prices are back up, led by steel prices

- Mechanical and electrical materials prices may have passed their peak

- Cost of running construction plant is up due to higher fuel costs

4. Key indicators

Percentage change (April 10 to April 11) %

Consumer prices index 4.5

CPI has now been above the government target of 2% for 17 consecutive months and 4% or higher since January. January’s rise in VAT was estimated by the Office for National Statistics to have added 0.76% to the index. The retail prices index continues to record a higher rate of inflation, 5.2% in April.

Industry input costs

- Materials and fuels purchased by manufacturing industry 17.6

- Materials and fuels purchased by manufacturing industry excluding food, beverages, tobacco and petroleum industries (FBT&P) 12.2

The increase in input costs is at its highest since September 2008, driven in large part by the rise in oil prices, up 38% over the last

12 months.

The index surged 2.6% in April alone. Excluding the food, beverages, tobacco and petroleum industries (FBT&P), other industries’ input costs still rose 12.2% over the last year, double the rate of six months ago. In particular, industry has suffered from the following price increases:

- Electricity +3.7%

- Gas +51.8%

- Imported metals +17.7%

- Wood and wood products +3.3%

Industry output prices

- Output prices of manufactured products 5.3

- Output prices of manufactured products excluding FBT&P 3.4

There is an ever widening gap between industry input costs and output prices. Output prices are rising but at a much reduced rate compared to input costs.

Metals prices

Metals prices rose strongly from last June as the global economy picked up. But political uncertainties including unrest in the Middle East put a break on the trend and most metals prices have seen some retrenchment during the spring.

Percentage change (May 10 to May 11) %

- Copper +27

- Aluminium +26

- Lead +21

- Zinc +7

- Nickel +9

- Source: LME cash prices

Construction industry

Materials price increases for the construction industry over the last year are detailed below:

April 2010-April 2011 %

Construction materials generally:

- New housing +7.5

- Non-housing new work +10.2

- Repair and maintenance +8.8

Overall construction materials prices rose by 9.3% over the year to March 2011, increasing sharply since last December, in large part due to a renewed surge in steel prices.

Mechanical services materials:

- Housing only +6.9

- Non-housing +7.2

- Electrical services materials +6.2

Mechanical and electrical services materials prices accelerated at the turn of the year, reaching annual inflation rates of 9% and almost 11% respectively, in response to steel and copper price increases. Over the last month or two prices have moderated a little as metal prices have fallen.

Materials showing the most significant price movement variation from the average over the last 12 months are shown below:

April 2010 - April 2011 %

- Gas oil fuel 29.7

- Steel sheet piling 24.9

- Structural steel 21.2

- Electric wires and cables 19.9

- Kitchen furniture 1.4

- Cement 0.8

- Plastic sanitaryware 0.8

- Bricks and clay products 0.0

- Ceramic tiles 0.0

- Ready-mixed concrete -1.6

(Data sources: ONS and BIS. April 2011 figures provisional)

The increase in the price of gas oil fuel for construction plant reflects the rise in oil prices that occurred from last October before its recent slippage. Steel products reflect the increase in world steel prices that occurred in the first few months of the year. The decline in concrete prices reflects the difficult economic conditions faced by the construction industry.

Labour: Average construction earnings buck the national trend with a 1.4% decline

5. Labour market statistics

- Average earnings throughout the whole economy in Great Britain in the first three months of 2011 were 2.3% higher than last year

- Average earnings in construction over the same period declined by 0.9%

- Average pay in construction in March 2011 was £546 per week

- The number of construction jobs recorded in the fourth quarter 2010 was 2,128,000, down 246,000 on the recent peak in the third quarter of 2008

6. Wage agreements

Plumbers in England and Wales started the year by securing a 3% wage increase from 3 January but their colleagues in Scotland and Northern Ireland will have to wait until 6 June to receive a more lowly 2% rise, their first increase for two years.

Electricians in England and Scotland benefited from a wage increase in January 2010 and have so far been unable to agree any increase in terms for 2011.

�ڶ����� and civil engineering operatives

Operatives employed under the Working Rule Agreement of the Construction Industry Joint Council have seen their wage rates frozen since June 2008. Negotiations are currently under way between the employers’ and employees’ sides regarding a possible increase for 2011/12.

It is unlikely that any increase will be agreed for the normal anniversary date of the end of June but there are hopes of a small wage rise later in the year.

The �ڶ����� and Allied Trades Joint Industrial Council (BATJIC):

The 2010-2011 BATJIC wage agreement that came into effect on 13 September 2010 was supposed to last only until 12 June 2011.

But agreement has been reached between the Federation of Master Builders and the Unite union that extends that agreement until 12 September 2011, when basic hourly rates of pay will increase by 1%. Skill rates, apprentice rates and benefits will remain unchanged.

Plumbers - Scotland and Northern Ireland

The Joint Industry Board for the Plumbing Industry in Scotland and Northern Ireland agreed in January 2010 that rates of pay and allowances would be frozen until June 2011 when all rates and allowance would rise by 2%.

From 6 June 2011, the following basic rates of pay come into effect:

Rate per hour:

- Plumber, domestic heating fitter and gas service fitter £11.32

- Advanced plumber, advanced heating fitter and gas service engineer £12.89

- Technician plumber and gas services technician £14.28

- Plumbing labourer £10.10

The overtime threshold has been progressively reduced from 43 hours in 2009 to 40 hours from 6 June 2011.

No comments yet